2018 Indiana Forest Products Price Report and Trend Analysis

Survey Procedures and Response

Data are collected twice a year, but log prices change constantly. Standard appraisal techniques by those familiar with local market conditions should be used to obtain estimates of current market values for stands of timber or lots of logs. Please note, because of the small number of mills reporting logging costs, “stumpage prices” estimated by deducting the average logging and hauling costs from delivered log prices must be interpreted with extreme caution and are meant to only serve as a guide. Actual stumpage values you may be offered depend on many variables, such as access, terrain, time of year, etc.

Data for this survey were obtained by a direct mail and email survey to a variety of forest-product industries, including sawmills, veneer mills, concentration yards, and independent log buyers. Only firms operating in Indiana were included. The survey was conducted and analyzed by the Indiana DNR Division of Forestry (DoF). The prices reported are for logs delivered to the log yards of the reporting mills or concentration yards. Thus, prices reported may include logs shipped from other states (e.g., black cherry veneer logs from Pennsylvania and New York).

The survey was mailed to 17 firms and emailed to 31 firms. It is estimated these companies produce close to 90% of the state’s roundwood production. Electronic reminders, follow-up phone calls and additional mailings encouraged responses.

A total of 21 firms reported some useful data. Five mills reported production of 5 MMBF or greater. Total board-foot production reported for 2017 was 57 MMBF compared to 70 MMBF for 2016, and 42 MMBF for 2015. The largest single-mill production reported was 21 MMBF. These annual levels are not comparable because they do not represent a statistical estimate of total production.

The price statistics by species and grade don’t include data from small custom mills, because most do not purchase logs, or they pay a fixed price for all species and grades of pallet-grade logs. They are, however, the primary source of data on the cost of custom sawing and pallet logs. The custom sawing costs reported do not reflect the operating cost of large mills.

This report can be used as an indication of price trends for logs of defined species and qualities. It should not be used for the appraisal of logs or standing timber (stumpage). Stumpage price averages are reported by the Indiana Association of Consulting Foresters in the previous issue of the Indiana Woodland Steward.

Delivered Sawlog Prices

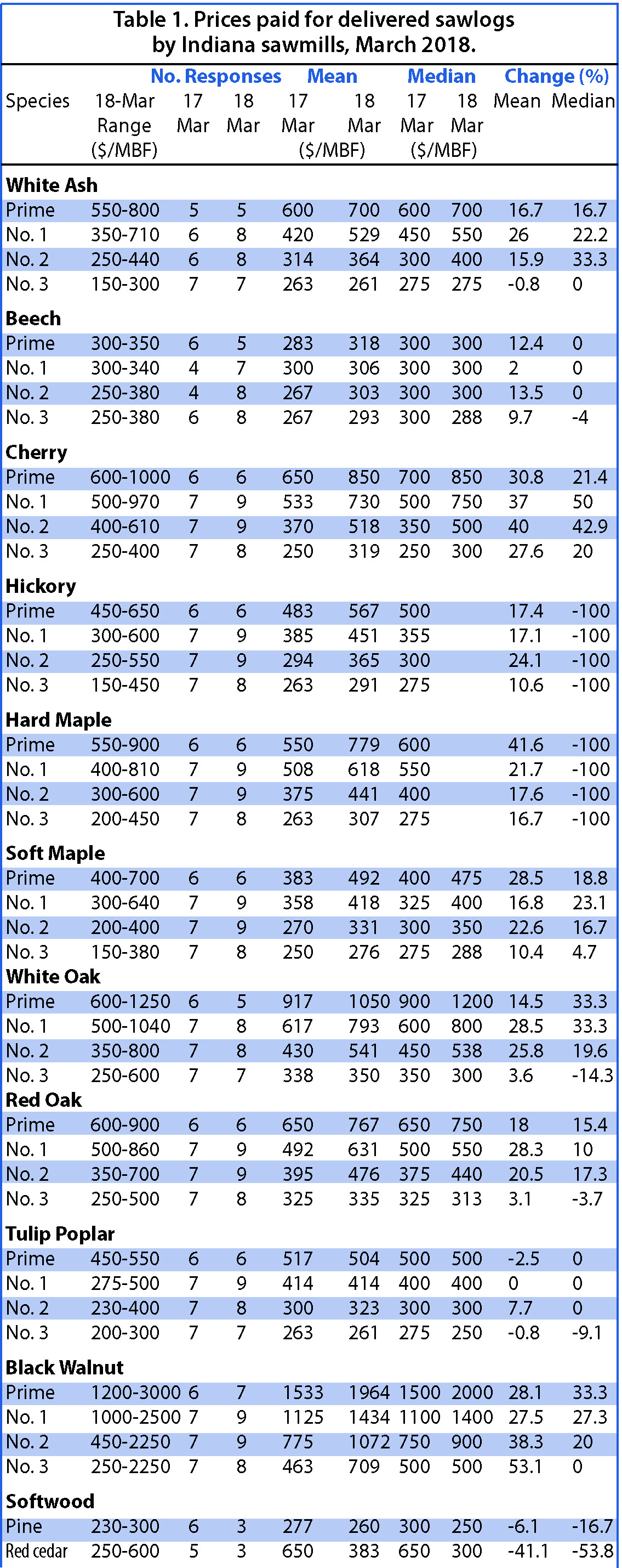

The number of mills reporting delivered sawlog prices was slightly higher than those who reported in the 2017 spring report (Table 1). Sawlog prices for the premium species (specifically black walnut and white oak) were up significantly from the 2017 spring report. Black walnut prices were up across all grades by 37%. White oak log prices were up as well by 18% compared to the 2017 spring report. From an overall standpoint, prices were up for every species except softwood (pine and cedar). Overall, across all species and grades, prices were up 19% from the 2017 spring price report.

Premium Species

White oak sawlog prices were up across all grades. Grades #1 and 2 saw the biggest jump, with prices 28% and 20% higher, respectively. Prime log prices were up 14%, while #3 grade logs experienced the smallest increase at almost 4%. White oak sawlog prices were down across all grades. Prime sawlog prices were off 3.5%, grades 1-3 white oak sawlogs were down an average of almost 5%. Demand from overseas buyers for white oak logs is extremely strong. Stave log demand, while steady, is not quite what it was a year ago.

Demand for black walnut sawlogs is strong for the export markets, while demand is steady from domestic buyers. #2 and 3 grade walnut logs saw the largest increase at 38% and 53%, respectively. Overall, walnut log prices across all grades were 37% higher.

Red oak sawlog prices were higher across all grades, compared to the 2017 spring report. Prime sawlog prices were 18% higher while grade #1 and 2 sawlog prices averaged 24% higher. Grade # 3 sawlog prices saw the lowest increase of 3%.

Black cherry sawlog prices have probably made the largest turnaround of any hardwood species. This is primarily due to what seems like an unsatisfied demand from China as well as increased demand domestically. Cherry sawlog prices were up across all grades by almost 34%. Grade #2 sawlogs saw the largest increase, at 40%, while #1 grade sawlog prices were 37% higher than what was reported in the 2017 spring report.

Hard maple sawlog prices followed the same trend as the rest of the hardwood species. Prices were higher across all grades by 24%. Prime hard maple logs saw the largest increase at 42%, while the grade sawlog increases were more moderate.

Soft maple sawlog prices were higher across all grades by almost 20%. Prime soft maple logs had the largest increase of 28.5% compared to the 2017 spring report. Grades #1- 3 sawlog prices averaged just over 16% higher.

Other Hardwood Species

The emerald ash borer continues its path of destruction across Indiana. Many experts say that within five years there will be few to no ash trees left. Landowners are trying to harvest their ash before the quality deteriorates. The export market for ash is still good. Several exporters are looking for 150-plus containers per months to meet their demand. Sawlog prices across all grades averaged 14% higher than during the spring of 2017. Grade #1 sawlogs had the largest increase, 26%. Grade #3 sawlogs were one of only three items that had a price decrease.

Tulip poplar sawlog prices were almost identical to those was reported during the 2017 spring report. Prices were up across all grades by only 1%. Prime and #3 grade sawlog prices were down by 2.5% and 1%, respectfully.

Softwood Logs

The price of pine sawlogs decreased by 6% to $260 MBF, while red cedar prices were off by a reported 41%. It should be noted that only three producers reported pine and cedar pricing.

Veneer Log Prices

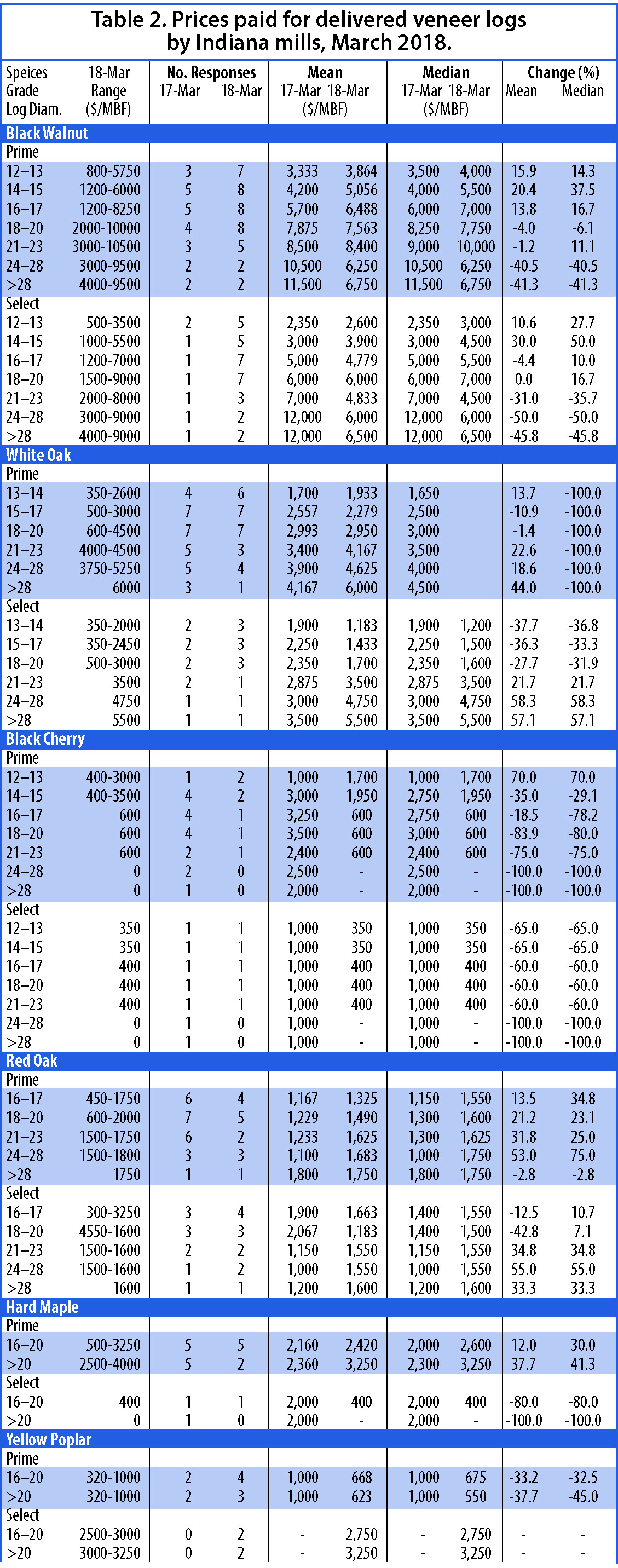

The number of mills reporting veneer-log prices increased slightly from the 2017 spring pricing report (Table 2). Prices were reported by both veneer mills and sawmills. Sawmills resell their veneer-quality logs to veneer mills, exporters, overseas importers and manufacturers. On occasion, sawmills may produce specialty cuts like quarter sawn with the marginal veneer logs. The variation in veneer log pricing is due to mix-veneer mills, sawmills and loggers reporting their values. This difference in values could be reduced if prices were only from veneer manufacturers.

Overall, market comments seem positive. Walnut and white oak continue to be highly sought after, primarily due to a very strong export market. Many veneer-log producers are sold out of both of these species. Whether you support or oppose log exporting, it is a large segment of the log sales. Current more-stringent phytosanitary requirements as well as increased enforcement of those existing rules in China have slowed the log exports, but most in the industry feel this situation will not be drawn out, long term. However, it remains to be seen how China will react to President Trump’s tariffs being imposed on China. Pricing remains very competitive from the export (especially China) side. Overseas veneer companies continue to process North American veneer logs. Wood lookalikes of plastic and vinyl as well as the ability to use high-quality 3D images continues to be a major concern for the veneer business. Most consumers would have a hard time distinguishing between the lookalikes and real wood. Those manufacturers can make the plastic and vinyl look exactly like wood but with a cheaper price.

Black walnut and white oak veneer remain in steady to strong demand both domestically and internationally. In addition to the demand from the veneer markets, white oak is still sought after by stave log buyers. Black walnut veneer log prices were higher for the prime smaller diameter logs. Larger diameter prime veneer-log prices were off as much as 40%. Overall, prices for prime black walnut were 5% lower. The same trend followed for the walnut select-veneer logs. Smaller-diameter veneer-log prices were higher, while the larger diameter log prices were reported to be lower than what was reported in the 2017 spring report. Black walnut veneer-log prices (prime and select) were 9% lower than in the spring of 2017.

White oak prime veneer-log pricing was higher for this report. Prime white oak veneer-log pricing across all diameters was 14% higher, while select white oak veneer log pricing was almost 6% higher. With white oak, the larger diameter prime and select veneer-log pricing saw the biggest increases. Prime white oak veneer logs >28” saw a 44% increase in pricing, while select white oak veneer logs from 21 inches d.b.h. and higher averaged 45% higher than reported in the spring of 2017.

Cherry veneer log markets continue to be very slow. The lion’s share of demand for cherry is for common-grade lumber, with China as the main destination, so cherry veneer logs are just not in high demand. Prime cherry veneer log pricing was off by 57%, and the select cherry veneer log pricing was down almost 73%. It is worth noting, however, that only one of two producers provided pricing information for cherry.

Red oak prime veneer-log prices rebounded significantly from those in the 2017 spring report. Prime red oak veneer-log pricing was 17% higher across all diameters, while select red oak veneer log prices were up 13.5% across all diameters. Prime red oak logs in the 24-28 d.b.h. class saw the biggest increase, 53%. Select red oak veneer logs between 24-28 d.b.h. were up 55% from the 2017 spring price report.

Veneer mills again reported significantly lower prices for hard maple. Prime veneer hard maple pricing was down an average 32%. Again, please note that only one to two producers reported pricing for hard maple veneer logs.

Miscellaneous Products

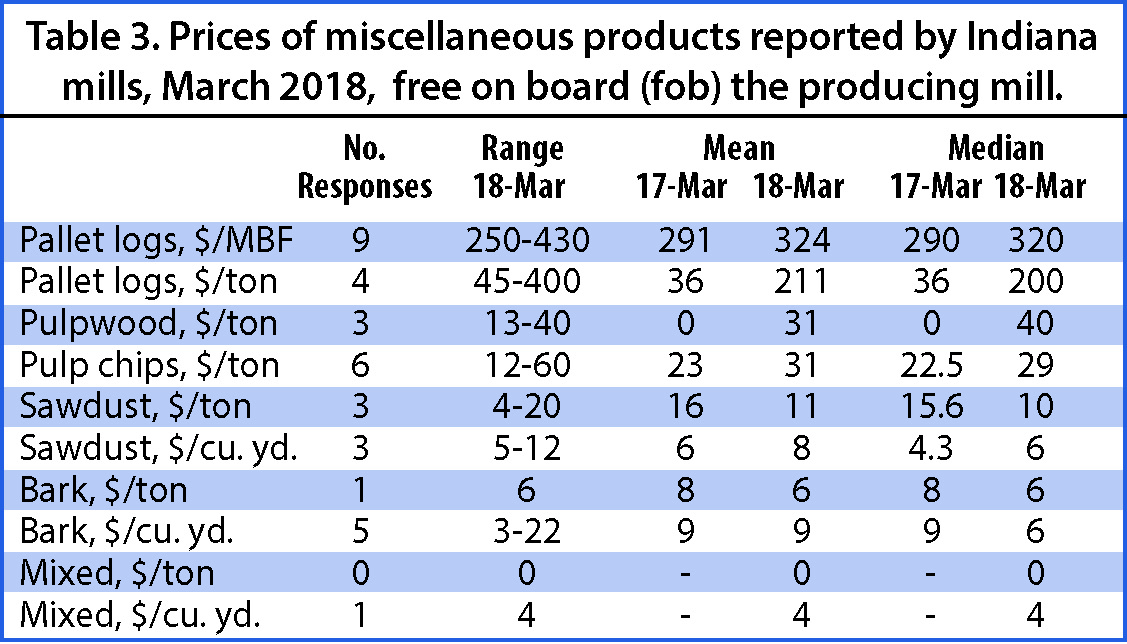

The change in prices paid for or received for various raw-wood products between the spring 2017 report and the current report are shown in Table 3. These are lower-quality and sometimes smaller logs purchased in batches of random species to be sawn into cants or chipped. The cants are re-sawn into boards used for pallets, blocking, railroad ties or other industrial applications that have a strong market. Some mills restrict purchases to specific species or exclude specific species, depending on the markets they sell to. Low-grade or industrial markets have increased significantly since mid- to late 2017 to the present, and demand for these products is very good. It has been said many times that the pulse of the hardwood market can be measured by the low-grade/industrial markets. The price for pallet and cant logs per MBF increased by 10%. Only one producer reported pulpwood pricing, $31/ton. Chip pricing per ton was up 26% from the 2017 spring report’s figure, while sawdust pricing per ton was lower. Bark pricing per ton was $2 lower for this report.

Until about the 1970s, sawdust, chips and bark would have been burned or landfilled by many mills. They now have many more uses. Sawdust can be used to make fuel pellets, burned as a heating source, or used as animal bedding. Wood chips are produced primarily from slabs sawn off of debarked logs and are used in mulch, wood pellets, hog fuel, and animal bedding. The decline in the pulp and paper industry threatens this market. Bark used for landscape mulch is now a large market. In some facilities, all or some portion of these byproducts are used to fire efficient low-emission boilers to heat dry kilns year-round and heat facilities in the winter. Attempts have been made to cogenerate electricity at mills, standalone generating plants, and biofuel facilities. Success has been limited by the low cost of electricity purchased off of the grid, the below-cost price received if sold into the grid, and the high cost to produce biofuels.

Custom Costs

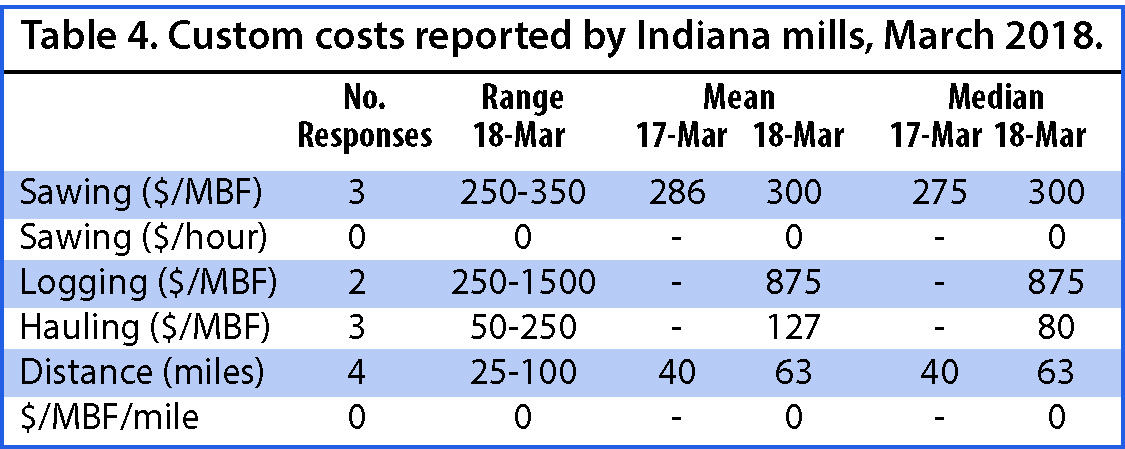

Costs of custom services increased from the spring report in the area of sawing (per/MBF). The high cost of diesel fuel usually plays a large role in logging costs as well as sale layout, topography, access, and costs to close out sales implementing Best Management Practices (BMPs) (Table 4). Custom-sawing costs were reported to be $300/MBF, an increase from $286 in the spring of 2017. There were very few surveys returned with logging and hauling costs, and there was a very wide range of pricing that appeared to skew average pricing. That being said, we feel those costs are generally around $200-$275 MBF, based on the items first mentioned in this section.

Timber Price Index

The delivered log prices collected in the Indiana Forest Products Price Survey are used to calculate the delivered log value of typical stands of timber. This provides trend-line information that can be used to monitor long-term prices for timber. The species and log-quality weights used to calculate the index are described in previous editions of this report. The weights are based primarily on the 1967 Forest Survey of Indiana, with changes made to remove basswood, cottonwood, elm, black oak and sycamore in 2014.

The nominal (not deflated) price is a weighted average of the delivered log prices reported in the price survey. The real prices are the nominal prices deflated by the producer price index for finished goods, with 1982 as the base year. The real price series represents the purchasing power of dollars based on a 1982 market basket of finished producer goods. It is this real-price trend that is important for evaluating long-term investments like timber and the log input cost of mills. Receiving a rate of return less than the inflation rate means that the timber owner is losing purchasing power, a negative real rate of return.

The nominal (not deflated) price is a weighted average of the delivered log prices reported in the price survey. The real prices are the nominal prices deflated by the producer price index for finished goods, with 1982 as the base year. The real price series represents the purchasing power of dollars based on a 1982 market basket of finished producer goods. It is this real-price trend that is important for evaluating long-term investments like timber and the log input cost of mills. Receiving a rate of return less than the inflation rate means that the timber owner is losing purchasing power, a negative real rate of return.

Note that each year the previous year’s number is recalculated using the producer price index for finished goods for the entire year. The price index used for the current year is the last one reported for the month when the analysis is conducted: April 2018. The index increased slightly from 1.91 for 2017 to 2.00 as of April 2018. Inflation in the 1 to 2 percent range is generally considered a sign of a healthy, growing economy. The change from 2017 to 2018 is about 2 percent.

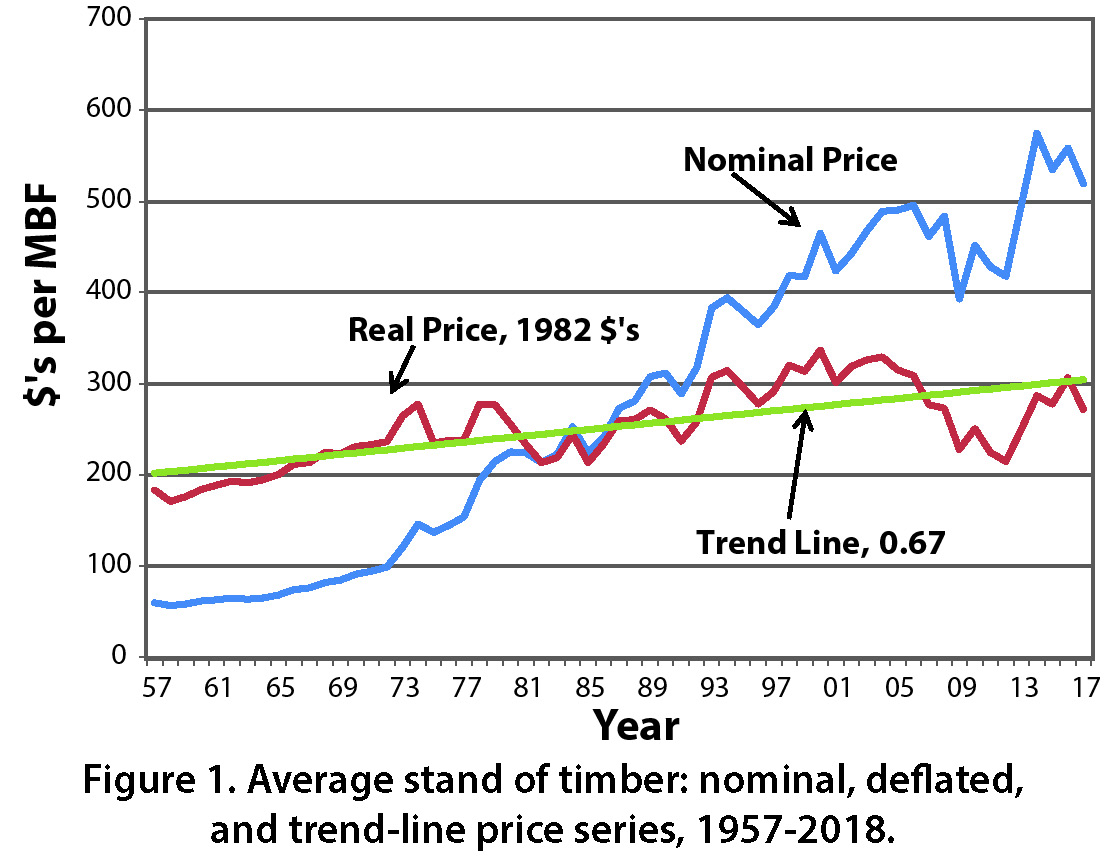

Average Stand

The nominal weighted average price for a stand of average quality increased from $519.7 in 2017 to $605.8 this year. Again, this series is based on delivered log prices, not stumpage prices. The deflated, or real price increased from $271.70 in 2017 to $302.90 this year. The average annual compound rate of interest required to take the linear trend line from $201 in 1957 to $302.90 in 2017 is 0.67 percent (Figure 1).

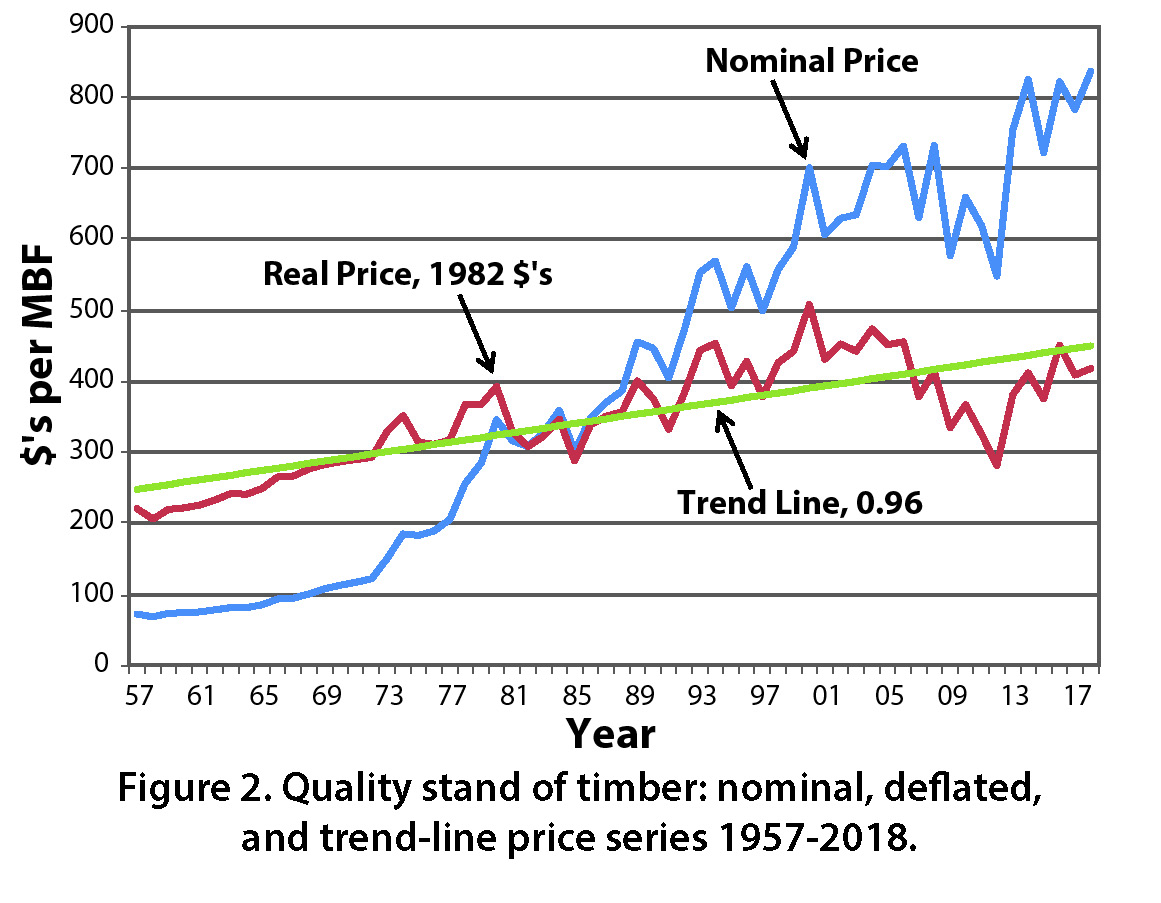

Quality Stand

The nominal weighted average price for a high-quality stand increased from $783.3 in 2017 to $837.2 this year. The average real price series for a high-quality stand increased from $409.5 in 2017 to $418.6 this year. The average annual compound rate of increase for the trend line is 0.96% per year (Figure 2).

Implications

The extent to which holding a stand of timber increases purchasing power depends on when you take ownership and when you liquidate. The 62-year period used in this analysis is much longer than the typical length of ownership. The rate of increase in the trend line doesn’t include the return resulting from increase in volume per acre by physical growth, nor the potential increase in unit price as trees get larger in diameter and increase in quality. Maximizing these increases in value requires timber management.

Jeffrey Settle is a Forest Resource Information specialist with the Indiana Division of Forestry. Chris Gonso is a Hardwoods Program Manager with the Indiana State Department of Agriculture.