2015 Indiana Forest Products Price Report and Trend Analysis

By Jeff Settle, Chris Gonso and Mike Seidl

Survey Procedures and Response

Data is collected twice a year, but log prices change constantly. Standard appraisal techniques by those familiar with local market conditions should be used to obtain estimates of current market values for stands of timber or lots of logs. Because of the small number of mills reporting logging costs, “stumpage prices” estimated by deducting the average logging and hauling costs from delivered log prices must be interpreted with extreme caution.

Data for this survey was obtained by a direct mail survey to a variety of forest products industries including sawmills, veneer mills, concentration yards, and independent log buyers. Only firms operating in Indiana were included. The survey was conducted and analyzed by the Indiana Division of Forestry. The prices reported are for logs delivered to the log yards of the reporting mills or concentration yards. Thus, prices reported may include logs shipped in from other states (e.g. black cherry veneer logs from Pennsylvania and New York).

The survey was mailed to 62 firms. It is estimated these companies produce close to 85-90% of the state’s roundwood production. Electronic reminders, follow-up phone calls and additional mailings got a few of those mills and operators back into the system.

Nineteen firms reported some useful data. Eight mills reported producing 1 million board feet (MMBF) or more. Four mills reported production of 5 MMBF or greater. Total production reported for 2014 was 64 MMBF compared to 147 MMBF for 2013, and 151 MMBF for 2012. The largest single mill production reported was 19 MMBF. These annual levels are not comparable since they do not represent a statistical estimate of total production.

The price statistics by species and grade don’t include data from small custom mills, because most do not purchase logs, or they pay a fixed price for all species and grades of pallet-grade logs. They are, however, the primary source of data on the cost of custom sawing and pallet logs. The custom sawing costs reported in Table 4 do not reflect the operating cost of large mills.

This report can be used as an indication of price trends for logs of defined species and qualities. It should not be used for the appraisal of logs or standing timber (stumpage). Stumpage price averages are reported by the Indiana Association of Consulting Foresters in the Indiana Woodland Steward, http://www.inwoodlands.org/.

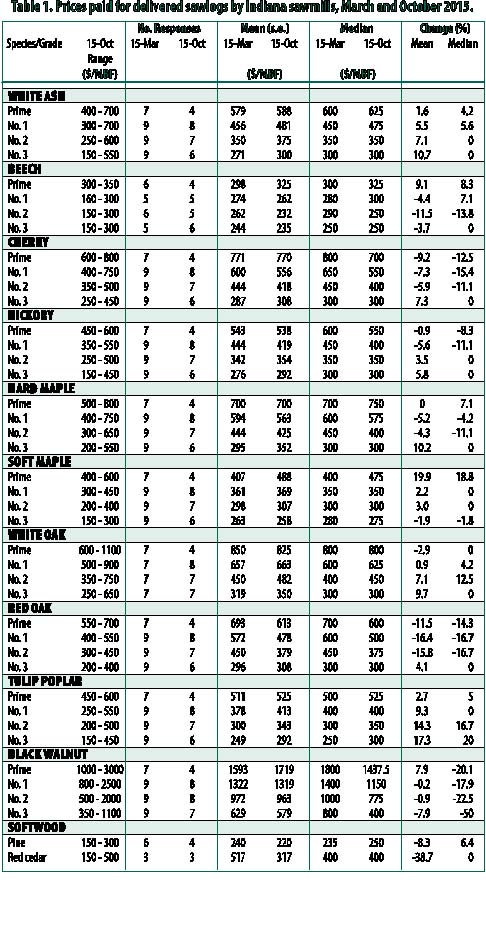

Delivered Sawlog Prices

The number of mills reporting delivered sawlog prices decreased only slightly from the earlier survey conducted in the spring of 2015 (Table 1). Sawlog prices for the premium species (specifically black walnut and white oak) were up slightly from the spring report. Almost without exception sawlog prices for the premium species, such as black walnut and white oak have increased. Overall prices were up for most of the other species.

Premium Species

Three of the four grades of white oak sawlogs increased in price with the exception being the prime grade. With the markets being so strong for veneer, stave, and rift/quartered logs, finding larger, quality logs has become quite a challenge. Prices being paid for red oak were down significantly from the spring report.

Demand for black walnut has slowed in recent months so availability is not the issue it was several months ago. Prime black walnut logs increased 8% while the remaining three log grades saw lower average prices.

Black cherry sawlog prices decreased around 4% across three of the four grades, the exception being No. 3 sawlogs which was 7% higher. Consumer demand for the darker finished wood has waned the past year and this is most likely the cause for lower log pricing.

Hard maple sawlog prices were generally down with the exception of the No. 3 grade sawlog. The summer and early fall months usually see less hard maple production due to the fear of stain and this may have played a large part in the price drops. Soft maple markets have been pretty steady due to strong lumber demand. Consumers are buying more painted wood materials which play very well into soft maple’s hands. Prime soft maple logs averaged almost 20% higher while the average price across the three remaining grades was basically unchanged.

Other Hardwood Species

Other Hardwood Species

More and more ash timber is being harvested in an effort to stay ahead of the Emerald Ash Borer. Production is high right now. That being said, ash sawlog prices still rose slightly (6%) compared to the spring report. The lower grade sawlogs saw significant price increases.

Tulip poplar increased across all grades except the prime grade. Normally when poplar markets are good, overproduction eventually slows the market. Poplar markets however have been one of the steadiest performers among hardwoods. Tulip poplar prices across all log grades averaged 11% higher from the spring 2015 report.

Softwood Logs

The price of pine sawlogs decreased slightly to $220/MBF. However, red cedar decreased 38% to $317/MBF. Four producers reported pine sawlog prices and three producers reported red cedar prices.

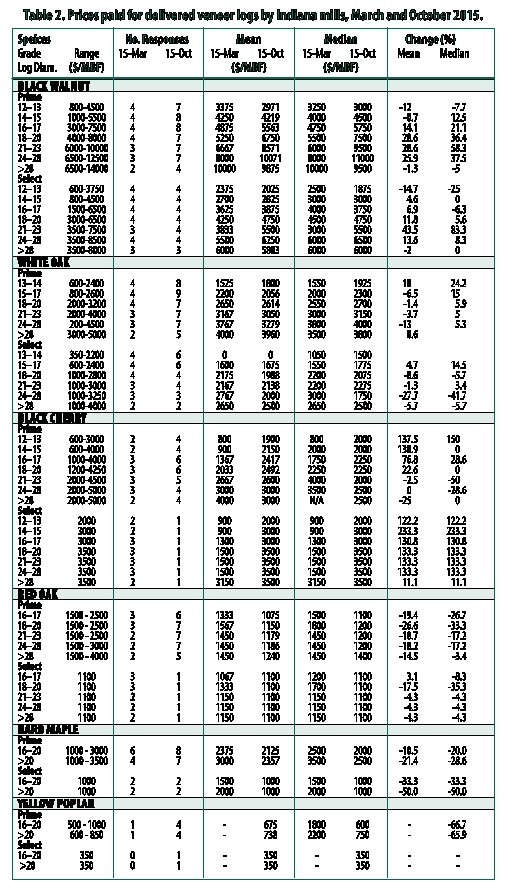

Veneer Log Prices

The number of mills reporting veneer log prices increased slightly from the spring 2015 report (Table 2). Prices were reported by both veneer mills and sawmills. Sawmills resell their veneer quality logs to veneer mills, exporters, overseas importers and manufactures. On occasion sawmills may produce specialty cuts like quarter sawn with the marginal veneer logs. The variation in veneer log pricing is due to mix veneer mills, sawmills and loggers reporting their values. This difference in values could be reduced if prices were only from veneer manufactures.

As reported in the spring, veneer demand remains slow with most mills running at 60% - 70% capacity. Conversely, veneer quality logs continue to remain in demand although pricing has leveled off or in some species have dropped this fall. Depending on the species, these decreases are greater in some, i.e. red oak than others like walnut. Additionally, weather conditions like the economic environment can play havoc on log pricing and volumes available.

Black walnut and white oak veneer remain in demand both domestically and internationally with pricing continuing for the most part remaining stable. Additionally, importers especially China are purchasing 3SC & 2SC walnut logs which has driven some of the local veneer mills and sawmills to drop out of the market or reduce production.

Veneer mills specializing in certain species (i.e., hard maple) report to some extent higher pricing mostly due to the larger volumes and freight costs to the mill. Overall this domestic demand for veneer, 3SC, 2SC, and grade 2 and 3 saw logs continues to keep pricing stable. Additionally, a slower economic condition throughout the international markets also increases the pressure on export log value and should continue into 2016.

These economic conditions will also affect white oak veneer, but to a much smaller degree. One of the biggest drivers for white oak currently is the stave market. Wine and whiskey manufactures are currently having difficulty building inventories thus requiring additional stave demand. When you add the demand for quarter-sawn and export lumber to the mix, the pressure for logs increases exponentially. Look for white oak logs to remain constant for 2016 and possibly longer.

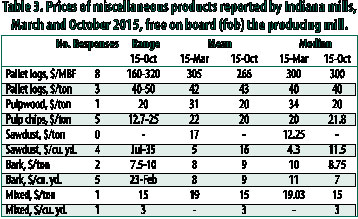

Miscellaneous Products

The change in prices paid for or received for various raw-wood products between the spring 2015 report and the current report. (Table 3). These are lower quality and sometimes smaller logs purchased in batches of random species to be sawn into cants or chipped. The cants are re-sawn into boards used for pallets, blocking, railroad ties or other industrial applications that have a strong market. Some mills restrict purchases to specific species or exclude specific species, depending on the markets they sell to. The price for pallet and cant logs decreased slightly, pulpwood and bark prices generally decreased, and sawdust prices increased from the spring report.

Until about the 1970’s sawdust, chips and bark would have been burned or landfilled by many mills. They now have many more uses. Sawdust can be used to make fuel pellets, burned as a heating source, or used as animal bedding. Wood chips are produced primarily from slabs sawn off of debarked logs. The decline in the pulp and paper industry is a threat to this market. Bark used for landscape mulch is now a large market. In some facilities all or some portion of these byproducts are used to fire efficient low-emission boilers to heat dry kilns year round and heat facilities in the winter. Attempts have been made to cogenerate electricity at mills, standalone generating plants, and biofuel. Success has been limited by the low cost of electricity purchased off of the grid, below cost price received if sold into the grid, and the high cost to produce biofuels.

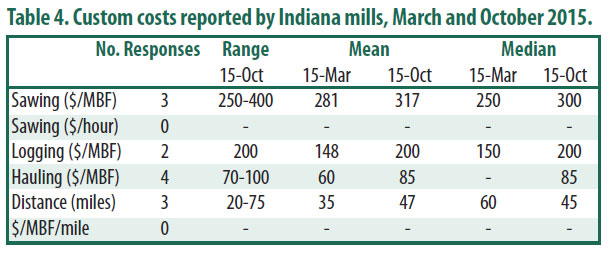

Custom Costs

Costs of custom services increased from the spring report in the areas of sawing and logging (per/MBF). The high cost of diesel fuel usually plays a large role in logging costs. (Table 4). Logging costs as reported in this survey indicate an increase in average logging costs from $148 to $200

per MBF.

Indiana Timber Price Index

The delivered log prices collected in the Indiana Forest Products Price Survey are used to calculate the delivered log value of typical stands of timber. This provides trend-line information that can be used to monitor long-term prices for timber. The weights are based primarily on the 1967 Forest Survey of Indiana. The following species were removed from the index and their relative weight reassigned proportionally to the remaining species in both average and quality stands: basswood, cottonwood, elm, black oak and sycamore.

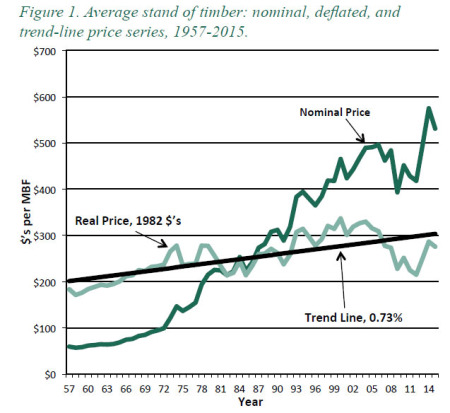

The nominal (not deflated) price is a weighted average of the delivered log prices reported in the price survey. The price indexes are the series of nominal prices divided by the price in 1957, the base year, multiplied by 100. Thus, the index is the percentage of the 1957 price. For example, the average price in 2014 for the average stand was 937.0 percent of the 1957 price. The index for a quality stand increased from 997.5 percent to 1092.6 percent.

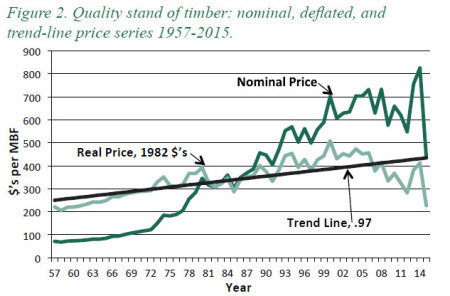

The nominal (not deflated) price is a weighted average of the delivered log prices reported in the price survey. The price indexes are the series of nominal prices divided by the price in 1957, the base year, multiplied by 100. Thus, the index is the percentage of the 1957 price. For example, the average price in 2014 for the average stand was 937.0 percent of the 1957 price. The index for a quality stand increased from 997.5 percent to 1092.6 percent.

The real prices are the nominal prices deflated by the producer price index for finished goods, with 1982 as the base year. The real price series represents the purchasing power of dollars based on a 1982 market basket of finished producer goods. It’s this real price trend that is important for evaluating long-term investments like timber and the log input cost of mills. Receiving a rate of return less than the inflation rate means that the timber owner is losing purchasing power, a negative real rate of return.

Note that each year the previous year’s number is recalculated using the producer price index for finished goods for the entire year. The price index used for the current year is the last one reported for the month when the analysis is conducted: November this year. The index decreased from 200.5 for 2014 to 192.7 as of November 2015.

The nominal weighted average price for a stand of average quality decreased from $575.10 in 2014 to $531.4 this year. Again, this series is based on delivered log prices, not stumpage prices. The deflated, or real, price increased from $286.8 in 2014 to $275.8 this year. The average annual compound rate of interest required to take the linear trend line from $201 in 1957 to $303 in 2015 is 0.72 percent, i.e. less than 1 percent (Figure 1). This rate will continue to decrease until the real price is above the trend line for several years.

The nominal weighted average price for a high-quality stand decreased from $825.9 in 2014 to $437.3 this year. The average real price series for a high-quality stand decreased from an adjusted $411.9 in 2014 to $226.9 this year. The average annual compound rate of increase for the trend line remained relatively unchanged at 0.97% year (Figure 2). As for an average stand, this rate will continue to decrease until the real price is above the trend line for several years.

Implications

The extent to which holding a stand of timber increases purchasing power depends on when you take ownership and when you liquidate. The 59 year period used in this analysis is much longer than the typical length of ownership. The rate of increase in the trend line doesn’t include the return resulting from increase in volume per acre by physical growth, nor the potential increase in unit price as trees get larger in diameter and increase in quality. Maximizing these increases in value requires timber management.

The complete 2015 Indiana Forest Products Price Report and Trend Analysis can be read in its entirety at: www.in.gov/dnr/forestry/.

Jeffrey Settle, Forest Resource Information (FRI); Chris Gonso, Ecosystem Services Specialist for the Indiana Department of Natural Resources, Division of Forestry; and Mike Seidl, Hardwoods Program Manager for the Indiana State Department of Agriculture